Summary

Stablecoins – cryptocurrencies pegged 1:1 to stable assets like the U.S. dollar – are emerging as the internet’s next-generation payment rails, enabling near-instant and low-cost global transfers without traditional intermediaries. They have the potential to reduce cross-border fees by up to 80–90% compared to banks or wire services, opening up new digital business models such as micropayments and streaming payments. When people say that there is no direct use case for blockchain/crypto, this is by far the easiest thing to point them towards (at which point you can politely decline to further the conversation because it is not typically engaged in good faith).

Stablecoins – cryptocurrencies pegged to stable assets like the U.S. dollar – promise to be an open, global value transfer system, consistent with the original promises of the internet. By operating on public blockchains, stablecoins create a native internet payment layer where value moves as freely as information.

From Bank Wires to Borderless Wallets: Stablecoins as Internet-Native Money

Traditional electronic payments rely on a convoluted chain of intermediaries – point-of-sale networks, payment processors, correspondent banks, card networks, and more – each adding cost, delay, and points of failure. This “Rube Goldberg machine” of intermediaries results in exorbitant fees and slow settlement, especially across borders. For example, international B2B payments can take 3–7 days to clear and cost $14–$150 per $1,000 sent, with up to five different intermediaries each taking a cut. Even a simple $200 remittance can incur around 6.6% ( ~$13 ) in fees on average. These legacy frictions effectively act as a regressive tax on global commerce and financial inclusion, disproportionately burdening smaller businesses and the world’s poorest workers.

Stablecoins as a Payments Alternative

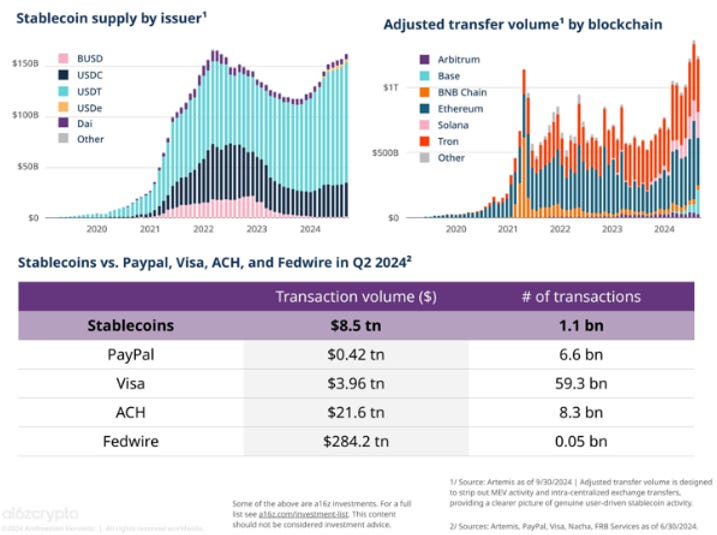

Just as anyone can send an email without asking permission from an email “gatekeeper,” two parties can transact in stablecoins without needing correspondent banks or payment processors to broker the transfer. Value transmits peer-to-peer via blockchain networks. The result is dramatically lower fees and near-instant settlement. In 2024, stablecoins moved trillions in value globally at a fraction of the cost of traditional methods – over $15 trillion for the year, effectively matching Visa’s annual payment volume. Notably, in the second quarter of 2024 alone, stablecoins facilitated $8.5 trillion in transactions across 1.1 billion on-chain transfers, more than double Visa’s $3.9 trillion volume in the same period. This surge is a strong signal that stablecoins have achieved product-market fit as a “killer app” for fast, borderless payments.

Major companies are already tapping into this internet-native money network. Multinationals like SpaceX use USD stablecoins to manage treasury across countries with volatile currencies (e.g. Argentina, Nigeria), effectively leapfrogging local banking limitations. Tech firms such as ScaleAI pay global contractors in stablecoins to avoid international wire delays. And fintech platforms like Stripe have integrated stablecoin payouts, enabling merchants to receive funds with only a 1.5% processing fee – about half the cost of traditional card payments. Unlike the siloed financial networks of the 20th century, stablecoins are global by default. Once value is tokenized as a stablecoin, it can flow to any internet-connected wallet in the world with no need to negotiate separate banking arrangements in each jurisdiction. In short, stablecoins are positioning themselves as the internet’s neutral, interoperable money layer – the financial equivalent of how TCP/IP enables open data exchange.

Cross-Border Payments at the “WhatsApp Moment”

Not long ago, sending a text message abroad cost cents per message and often failed to deliver. Then internet-native messaging (e.g. WhatsApp) made global texting instantaneous and free. Today, payments are where messaging was circa 2008 – fragmented by borders and hamstrung by high fees – and stablecoins are poised to do for money what WhatsApp did for communication. Nowhere is this more evident than in cross-border transfers and remittances, where the inefficiencies of legacy systems are most acute.

A stark illustration is the cost of remittances: Sending $200 from the U.S. to Colombia via traditional methods incurs about $12 in fees on average. In contrast, using a dollar stablecoin on a blockchain, the network fee for the same transfer is pennies – sometimes around $0.01. Even after accounting for converting the stablecoin into local currency (which might add a few percentage points in exchange fees, depending on the service), the total cost is still markedly lower, and it’s dropping as crypto on-ramps become more competitive. In practice, stablecoin remittances can reduce fees by ~80–90% compared to banks or money transmitters, while delivering funds to the recipient within minutes rather than days. This efficiency has real human impact, effectively putting more money into the pockets of migrant workers’ families and small businesses in emerging markets.

Why are stablecoin transfers so much cheaper and faster? The public blockchain infrastructure underpinning stablecoins has seen massive scaling improvements. Transaction costs on networks like Ethereum have plunged by over 99% with the advent of Layer-2 scaling solutions. For example, the average gas fee to send USDC (a popular USD stablecoin) on Ethereum’s base layer fell from ~$12 in 2021 to about $1 by September 2024, and on efficient Layer-2 networks like Base, it’s now <$0.01. These technical advances make it economically feasible to send even tiny payments across the globe. An international bank wire, by comparison, costs around $44 on average and often isn’t practical for small-value transfers. Stablecoins thus open the door to micropayments and new digital business models that traditional fees would have rendered impossible – for instance, streaming a few cents at a time to content creators or IoT devices paying each other for services. Legal advisors should note that this borderless programmability introduces novel scenarios (machine-to-machine payments, pay-as-you-go digital services, etc.) which existing financial regulations never contemplated.

The cost to send money internationally has plummeted with blockchain-based stablecoins. As shown above, sending USD via stablecoin (USDC) on modern networks can be done for fractions of a cent in fees, a drop of over 99% from earlier on-chain costs and far below the ~$44 average fee of a traditional international wire. This dramatic cost reduction is enabling new payment use cases that were previously uneconomical.

By making cross-border transactions near-instant and essentially frictionless, stablecoins are creating a “level playing field” for global commerce. A startup in Bangalore can pay a freelancer in Lagos or purchase software from a vendor in Buenos Aires with the same ease as paying a local supplier. However, this globalization of money movement also means companies using stablecoins must navigate a patchwork of jurisdictions in real time. When value moves freely across borders without bank intermediaries, questions arise: Which country’s laws govern a given transaction? How do currency controls or sanctions apply when payments bypass traditional channels? These questions bring us to the critical role of emerging regulatory frameworks.

Regulatory Clarity: Unlocking Stablecoins’ Potential Across Jurisdictions

Financial regulators worldwide are now grappling with how to oversee stablecoins as they transition from a niche technology to an integral part of the financial system. Initially, many policymakers viewed crypto broadly with skepticism, focusing on risks and enforcement. But there is growing recognition that clear, tailored regulation of stablecoins can be a catalyst for mainstream adoption rather than a barrier. In fact, smart legislation is increasingly seen as the key to moving stablecoin innovation out of legal limbo and into the regulated financial mainstream. For legal practitioners, it’s crucial to stay abreast of these fast-evolving frameworks in all relevant jurisdictions:

- United States: The U.S. does not yet have a comprehensive federal law for stablecoins, but momentum is building in Congress to establish one. Lawmakers on both sides of the aisle have introduced bills to create a regulatory regime for “payment stablecoins” – a regime that would likely require issuers to fully back their coins with high-quality liquid assets, undergo regular audits of reserves, and implement robust measures against illicit finance. Such legislation is expected to mandate registration or licensing for stablecoin issuers (potentially under bank-like supervision or a new federal license category) to ensure consumer confidence and financial stability. As of early 2025, Congress is hashing out details, but the mere prospect of clear rules is already encouraging more institutions to explore stablecoin use. U.S. regulators have also hinted at allowing decentralized stablecoin innovation to flourish within bounds – preserving the ability of developers to create algorithmic or crypto-collateralized stablecoins that eliminate intermediaries, as long as risks are addressed. In the interim, U.S. companies working with stablecoins must navigate existing laws like state money transmitter licensing (for fiat-to-stablecoin exchanges or custodial wallets) and federal anti-money-laundering requirements, while keeping an eye on forthcoming federal standards.

- European Union: Europe has leapt ahead with a sweeping regulatory framework. The EU’s Markets in Crypto-Assets Regulation (MiCA) – the world’s first comprehensive crypto law – explicitly covers stablecoins (termed “e-money tokens” and “asset-referenced tokens” in the regulation). MiCA imposes prudential and conduct requirements on stablecoin issuers, such as capital reserves, liquidity management, segregation of reserves, and investor disclosure obligations. Issuers must be authorized by regulators in an EU member state, meeting compliance standards similar to e-money institutions. Since MiCA’s stablecoin rules began coming into force in 2024, they have already reshaped the European stablecoin market – prompting some unlicensed operators to exit or adapt and giving regulated players a clear framework to operate in all EU countries. For companies using stablecoins in the EU, MiCA provides greater legal certainty about which stablecoins are compliant and can be used for payments or settlement. It’s a double-edged sword: while it raises the bar for issuers (ensuring more trustworthy stablecoins), it also means businesses must ensure any stablecoin they integrate has the necessary approval for EU usage.

- United Kingdom and Other Jurisdictions: The UK has also been proactive, engaging the public and industry through consultations to develop its crypto asset regulations. The UK is expected to introduce rules for stablecoins used as payments, likely bringing them within the scope of electronic money regulations or a new bespoke regime, with an emphasis on financial stability and AML compliance. In other global financial centers like Singapore, Hong Kong, and Japan, regulators have issued guidance or licensing frameworks for stablecoin issuers in recent years (for example, Japan’s Payment Services Act was amended to allow licensed banks and trusts to issue stablecoins). These frameworks commonly require maintaining reserve assets equal to outstanding coin value and screening users for compliance. Meanwhile, some countries with strict capital controls or crypto bans remain wary of stablecoins’ dollarization effects. Legal advisors must therefore consider not only the primary jurisdiction of their client (e.g. U.S. or EU laws) but also any local laws in markets where the stablecoin might be circulated or exchanged. A stablecoin transaction can trigger regulatory oversight in multiple jurisdictions simultaneously – for instance, a U.S.-based company paying an overseas contractor might implicate U.S. sanctions rules, EU crypto-asset rules (if the contractor is in Europe), and the local laws of the contractor’s country.

Critically, the trend across major economies is toward treating licensed stablecoins as a legitimate part of the financial ecosystem rather than leaving them in a gray area. Policymakers increasingly acknowledge a strategic dimension: Private USD stablecoins may reinforce the dollar’s global role. Over 99% of stablecoin value in circulation is USD-denominated, dwarfing the share of the next largest currency (the euro at 0.2%). U.S. lawmakers have noted that well-regulated dollar stablecoins could extend American influence in the digital economy even as cash use declines. Likewise, other governments see an opportunity to shape the stablecoin market in line with national interests – whether by issuing their own central bank digital currencies (CBDCs) or by encouraging domestic fintech champions to issue compliant stablecoins. For legal practitioners, this means that stablecoin regulation is not static; it’s a moving target influenced by geopolitical and economic priorities. Companies should be prepared for periodic adjustments in rules (e.g. new licensing mandates or cross-border cooperation on oversight) as countries refine their approach. Engaging early with regulators or participating in public consultations can even be a strategic move for companies heavily invested in stablecoin-based business models.

Compliance and Risk Management in a Stablecoin World (KYC/AML)

One of the biggest challenges with using stablecoins as a payment layer is reconciling their open, pseudonymous nature with Know-Your-Customer (KYC) and Anti-Money Laundering (AML) laws. Public blockchains allow value to move freely between addresses without revealing the identity of the transacting parties – great for permissionless innovation, but a double-edged sword when it comes to illicit finance risks. Regulators are understandably focused on preventing stablecoins from being misused for money laundering, terrorist financing, sanctions evasion, or fraud. Any company transacting in stablecoins must build robust compliance controls to address these concerns.

Key considerations include:

- KYC for On/Off Ramps: Most jurisdictions require that when users convert fiat to stablecoins or vice versa (the “on-ramps” and “off-ramps”), the service provider conducts KYC verification. Practically, this means if your client integrates a stablecoin payment flow, they will likely use an exchange, bank, or payment processor partner at the conversion points. Those partners will need to be properly licensed (as money services businesses, e-money institutions, etc.) and perform customer due diligence. Ensure any API or service your platform relies on for handling stablecoins has compliant KYC processes in place. Even for pure stablecoin-to-stablecoin transfers, if your client’s platform provides a hosted wallet for users, your client may themselves be deemed a “Virtual Asset Service Provider” (VASP) that must implement KYC for its users under regulations in many countries.

- Ongoing Transaction Monitoring: Once users hold stablecoins, they can send them to any blockchain address. Companies should use blockchain analytics and monitoring tools to track transactions involving their wallets or platform. This helps detect red flags such as transfers to or from known illicit addresses (e.g. addresses sanctioned by the U.S. OFAC or associated with dark markets). Notably, major USD stablecoin issuers have the ability to blacklist and freeze tokens associated with illicit activity, which has happened in high-profile hacks and sanctions cases. While freezing by issuers is a last resort, it means funds tainted by crime might become inaccessible. From a legal standpoint, having monitoring in place not only is good practice for AML compliance but also helps protect the company’s assets and reputation (you don’t want to unwittingly facilitate a sanctioned transaction and then have the stablecoin issuer lock up your funds).

- Travel Rule and Reporting: Financial authorities globally are extending the “Travel Rule” (which requires transmission of sender and recipient identifying information for wire transfers) to crypto transactions. If a business is sending or receiving stablecoins on behalf of customers, it may fall under these rules. For example, the EU’s Transfer of Funds Regulation now covers crypto transfers, and other countries are implementing similar requirements in line with FATF guidance. Legal advisors should ensure that their clients have a plan to share required originator/beneficiary information when transacting with other VASPs, or at least not to fall foul of reporting thresholds. This might involve using compliant intermediaries or messaging protocols designed for crypto Travel Rule compliance.

- Licensing as a Compliance Strategy: In many cases, it may be simpler and safer for a tech company to partner with an entity that is already licensed and compliant, rather than directly handling all regulatory obligations. For instance, a fintech app that wants to offer users stablecoin wallets might integrate with a custodian or trust company that holds the stablecoins for users under their licensed entity. The trade-off is some control and decentralization, but it can offload heavy compliance lifting. Conversely, if the company chooses to self-custody and directly manage stablecoin flows, obtaining the necessary money transmitter licenses, registrations, or other authorizations in each jurisdiction is essential before scaling up transactions.

Overall, embedding compliance into the design of stablecoin-based services is non-negotiable. Regulators have made it clear that anti-money-laundering rules apply equally to crypto assets – the same expectations of “countering illicit finance” exist as in traditional finance. In fact, a future U.S. stablecoin law is likely to enshrine explicit AML program requirements for issuers and possibly certain wallet providers. The strategic upside is that well-regulated stablecoin ecosystems will gain trust and unlock more users (and more institutional adoption) over time. Legal teams should help their organizations balance the openness of blockchain technology with the controlled access points of compliance – achieving the benefits of permissionless payments without inviting enforcement actions. This might include advising on geo-fencing certain jurisdictions, setting transaction limits pending enhanced due diligence, or using whitelisted wallet programs for higher-risk corridors.

Settlement Finality, Custody, and Other Considerations

Shifting payments onto stablecoins doesn’t just change speed and cost – it also alters some fundamental assumptions in commercial transactions. Users (and the lawyers looking over their shoulders) have to reassess concepts like payment finality, custody of funds, and contractual risk allocation in the context of blockchain-based payments:

- Instant Settlement & Irreversibility: Unlike credit card or ACH payments, which can be reversed or disputed, a stablecoin transfer on a blockchain is typically irreversible once confirmed. In traditional finance, consumers have protections (chargebacks, error resolution processes) and businesses have clearing delays that allow cancellation of mistaken payments. With stablecoins, settlement is final within minutes of the transaction being mined into a block. There is no central operator to appeal to if funds are sent to the wrong address or if a payer fraudulently initiates a transfer. The only recourse is persuading the recipient to refund or, in cases of theft, law enforcement intervention. Legal advisors should ensure that contracts and terms of service reflect this reality – for instance, explicitly stating that payments in cryptocurrency are considered received when the applicable number of block confirmations is reached, and that the risk of providing an incorrect wallet address lies with the sending party. In high-value transactions, parties might agree on verification steps (like sending a small test amount first) or use an escrow smart contract to mitigate error risk.

- Settlement Finality and Legal Recognition: Another subtle point is how legal regimes view the finality of a blockchain transfer. Many countries have enacted laws for payment systems that ensure once a payment is settled in that system, it cannot be unwound even if a participant becomes insolvent. With stablecoins, there isn’t yet a universally recognized legal “finality” framework – it’s a matter of technical finality on the blockchain. Lawyers may need to consider including choice-of-law and dispute resolution clauses that account for the new payment medium. For example, if a stablecoin payment is used to discharge an obligation, under what law is that considered valid payment? One might specify that the parties treat a stablecoin payment as equivalent to a cash payment for all purposes of their contract. Additionally, because blockchain forks or network failures, while rare in major networks, are not impossible, one should contemplate how a fork (which could theoretically reverse transactions) would be handled. These are new wrinkles in commercial law that tech-savvy lawyers are beginning to ponder.

- Custody and Control of Funds: When a company holds stablecoins, the traditional definitions of “funds” and custody take on digital form. Possession of the private keys equals control of the assets. From a risk management perspective, businesses need to secure those keys with the highest rigor – using hardware security modules, multi-signature wallets, or professional custodians. The legal team should verify who within the organization has access to the wallets and implement controls (multi-factor approvals, dual controls for transfers) to prevent internal fraud or mistakes. If an outside custodian or bank is used to hold the stablecoins (in a custodial account or trust), the service agreement should clearly delineate ownership of the crypto assets, liability for loss (including through cyberattacks), and insurance coverage if available. A positive trend is that several jurisdictions are clarifying the legal status of crypto assets in custody (for example, defining them as customer property not part of a custodian’s estate in bankruptcy). Counsel should stay updated on these developments to advise on the safest way to hold significant stablecoin reserves.

- Licensing for Stablecoin Services: We touched on licensing from a regulatory compliance standpoint, but it bears repeating in the operational context. Activities like issuing a stablecoin, exchanging it for fiat, transmitting it on behalf of someone, or offering custody of stablecoins may trigger licensing in multiple jurisdictions. The absence of traditional banks in the loop doesn’t mean financial law obligations vanish – often, new licenses or registrations fill that gap. In the U.S., for example, if a tech company directly holds and transfers stablecoins for customers, it may need money transmitter licenses in many states (or partner with a licensed entity) until federal law changes. In the EU, that activity could make it a crypto-asset service provider under MiCA, requiring authorization and compliance with conduct requirements. When designing a stablecoin-integrated product, mapping out these regulated activities and either obtaining the needed licenses or structuring around them (e.g. non-custodial designs) is a critical strategic step. Early input from legal can save a company from inadvertent unlicensed operations down the road.

- Consumer Protection and Contract Terms: Companies offering stablecoin payment services should also consider consumer protection laws. If end-users are involved (e.g. a digital wallet for retail customers), there may be disclosure requirements about risks – such as the risk of losing private keys, volatility (if using non-USD stablecoins or algorithmic ones), and the lack of FDIC-style insurance. Terms of service should make clear that stablecoins are not bank deposits and outline whose responsibility it is to secure access. Additionally, clarity on fees (network fees, conversion fees) and timing (blocks sometimes take a bit longer to confirm) will prevent misunderstandings. Many legal systems do not yet have specific rules for crypto transactions under consumer law, but general principles (unfair contract terms, duty to act transparently) still apply.

So, while moving to stablecoin-based payments can streamline operations and open new markets, it requires retooling legal and operational frameworks that were built around reversible, intermediated transactions.

Strategic Takeaways

Stablecoins are becoming an integral part of the global financial architecture, blending the tech world’s ethos of open innovation with the heavily regulated realm of money. For legal practitioners advising tech or fintech firms, the key is to enable innovation while mitigating risk. Here are some strategic takeaways to guide your counsel on stablecoin initiatives:

- Harness the Efficiency – but Know the Mechanism: Stablecoins can dramatically reduce payment costs and settlement times for your clients. Leverage these benefits (e.g. for instant global payouts or treasury management) but ensure the business team understands how stablecoin transactions work. Educate stakeholders that sending value on-chain is fundamentally different from wiring money – it requires safeguarding private keys and accepting irreversible outcomes. This knowledge will inform smarter product design and risk controls.

- Map the Regulatory Terrain (No Surprises): Before deploying stablecoin-based services, map out the regulatory requirements in each jurisdiction of operation. Treat stablecoin flows like you would fiat flows from a compliance perspective. Check if the stablecoins in use are compliant or permitted in your target markets (e.g. MiCA-authorized in the EU). Identify any licensing needs early – whether money transmitter licenses, e-money licenses, crypto exchange registrations, or others – and plan whether to acquire these or partner with someone who has them. Proactively engaging with regulators or seeking legal opinions can clarify grey areas (for instance, if your use case might get an exemption or require a specific license).

- Build Embedded Compliance (KYC/AML by Design): Don’t bolt on compliance as an afterthought – integrate it into the user experience and backend from day one. This means designing onboarding processes to collect user information when needed, setting up transaction monitoring for suspicious blockchain activity, and having clear policies for handling anything that touches a sanctions list or darknet wallet. Regulators will expect controls “at least as good as” those in banking. Demonstrating a rigorous compliance program will also give prospective banking partners or regulators comfort that your stablecoin operations are responsible. In cross-border contexts, be mindful of each country’s AML rules – for example, if users in Country X can top-up or withdraw stablecoins, does Country X require you to register as a crypto asset service provider? These details matter for sustaining the service.

- Address Custody and Security Risks: Advising on stablecoins isn’t just about legal rules – it’s also about safeguarding digital assets. Work closely with your security teams to implement best practices for custody. Decide whether using third-party custodians (with appropriate legal agreements and insurance) makes sense versus self-custody. If the latter, treat the cryptographic keys as crown jewels: multilayered security, limited access, and contingency plans for key loss or compromise. Also, consider how the company will handle forks or technical issues on the blockchain network – have a policy for pausing transactions if needed, and communicate to customers how such events would be handled. These operational safeguards can prevent legal headaches (like customer lawsuits over lost funds) before they happen.

- Update Contracts and Disclosures: Whenever stablecoins become part of a business process, update the legal documentation accordingly. This includes customer agreements (acknowledging crypto risks and outlining responsibilities), partnership contracts (allocating who bears regulatory compliance duties or losses from technical failures), and internal policies. If, for example, your client is integrating stablecoins into a platform marketplace, ensure the user terms cover crypto payments and that there are procedures for dispute resolution since traditional chargeback paths won’t exist. Clarity and transparency here will preempt conflicts and build user trust.

- Stay Agile and Informed: The stablecoin space sits at the intersection of rapid technological innovation and rapidly evolving law. What’s legally permissible or best practice today may shift with the passage of a new law or an enforcement action tomorrow. Legal advisors should stay current on developments such as new legislation (e.g. a potential U.S. stablecoin act), changes in policy (like updated guidance from FINMA, MAS, or other regulators), and industry standards (for instance, emerging compliance protocols for DeFi transfers). Establish a process to re-evaluate the regulatory posture periodically – much like a financial institution would adjust to new regulations. And finally, consider engaging in industry groups or public consultations; many regulators are seeking input to craft balanced rules, and the voices of experienced tech lawyers can help shape frameworks that enable innovation while protecting consumers and markets.

Written by David Lopez Kurtz